Life Insurance Essentials

- -->> 5. Life Insurance Essentials

What you'll learn

Term Life InsuranceWhole Life InsuranceUniversal Life InsuranceChoosing the Right Policy

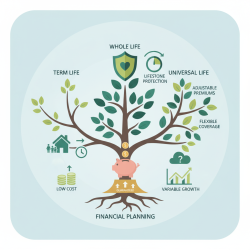

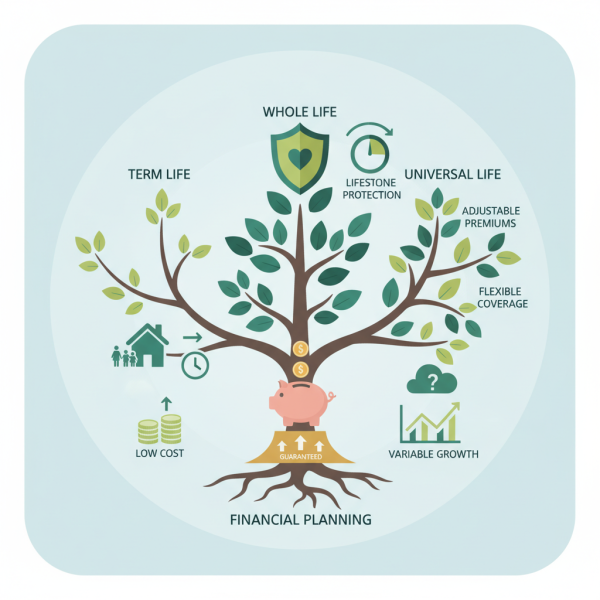

Term Life InsuranceWhole Life InsuranceUniversal Life InsuranceChoosing the Right PolicyLife insurance stands as a cornerstone of financial planning, offering a crucial safety net for your loved ones in the event of your untimely passing. Navigating the world of life insurance can often feel complex, with a variety of policy types each designed to meet different financial goals and life stages. Understanding these fundamental differences is essential for making an informed decision that aligns with your personal circumstances and provides the right level of protection for your family's future. This article will demystify the core offerings in life insurance: term, whole, and universal life policies, outlining their unique characteristics and benefits to help you choose wisely.

Understanding Term Life Insurance

Term life insurance is often considered the simplest and most straightforward form of life coverage. It provides protection for a specific period, or "term," such as 10, 20, or 30 years. If the insured person passes away within this term, their beneficiaries receive a predetermined death benefit. If the term expires and the insured is still living, the coverage typically ends, and there is no cash value payout.

One of the primary advantages of term life insurance is its affordability. Premiums are generally lower compared to permanent life insurance options, especially for younger, healthier individuals. This makes it an attractive option for those looking to maximize coverage during crucial periods, like when they have young children, outstanding mortgages, or significant debts. Term policies can often be renewed at the end of the term, though premiums will likely increase significantly due to age and health changes.

However, term life insurance does not build cash value over time. It is purely a death benefit product. Once the term concludes, if the policy is not renewed or converted, the coverage ceases. This aspect is important for individuals who might be seeking a policy that offers a savings component or lifelong coverage.

Exploring Whole Life Insurance

Whole life insurance represents a form of permanent life insurance, meaning it provides coverage for the entirety of the insured's life, as long as premiums are paid. Unlike term life, whole life policies come with a guaranteed death benefit and a cash value component that grows on a tax-deferred basis over time. This cash value can be accessed later in life through policy loans or withdrawals, offering a living benefit in addition to the death benefit.

The premiums for whole life insurance are typically level, meaning they remain the same throughout the life of the policy, providing predictability in budgeting. The growth of the cash value is also guaranteed, often at a modest rate set by the insurer. This predictability and the permanent nature of the coverage are significant advantages for those seeking long-term financial security and estate planning tools.

Key features of whole life insurance include:

- Guaranteed death benefit for life.

- Guaranteed cash value growth.

- Level premiums that do not increase.

- Ability to take policy loans or withdrawals from cash value.

- Potential for dividends from mutual insurance companies.

While offering stability and a savings component, whole life insurance premiums are considerably higher than term life premiums for the same death benefit amount, especially in the initial years. This higher cost is a trade-off for the guarantees and the lifelong nature of the coverage.

Delving into Universal Life Insurance

Universal life (UL) insurance is another type of permanent life insurance, but it offers more flexibility than whole life. UL policies also provide a death benefit and a cash value component, but policyholders have the ability to adjust their premiums and death benefit amount within certain limits. This flexibility can be appealing for individuals whose financial situations or coverage needs may change over time.

The cash value in a universal life policy grows based on an interest rate, which can be fixed or variable depending on the specific type of UL policy (e.g., guaranteed UL, indexed UL, variable UL). The interest rate credits to the cash value may fluctuate, introducing some variability compared to the guaranteed growth of whole life. Policyholders can often choose to pay more than the minimum premium, causing the cash value to grow faster, or pay less, drawing from the cash value to cover costs, though this risks policy lapse if the cash value depletes.

Benefits of universal life insurance include:

- Flexible premiums and death benefit options.

- Cash value growth linked to interest rates or market indexes.

- Potential to skip premium payments by using cash value.

- Provides lifelong coverage.

- Offers living benefits through cash value access.

The complexity and potential variability of universal life policies mean they require more active management and understanding from the policyholder. While flexibility is a strength, it also means there's a greater responsibility to ensure the policy remains funded adequately to avoid unintended lapse, especially if investment performance is poor or interest rates decline.

Key Factors When Choosing a Policy

Selecting the right life insurance policy requires careful consideration of several personal and financial factors. There is no one-size-fits-all solution, as the ideal choice depends heavily on individual circumstances. Key factors to evaluate include your current financial obligations, the number and age of your dependents, your long-term financial goals, and your budget for premiums.

Consider how long you anticipate needing coverage. If you only need protection for a specific period, such as until your children are grown or your mortgage is paid off, term life might be the most cost-effective solution. If you desire lifelong coverage, a savings component, or tools for estate planning, then permanent options like whole life or universal life would be more appropriate.

Your investment philosophy also plays a role. If you prefer guaranteed growth and simplicity, whole life might appeal. If you're comfortable with more variability for potentially higher cash value growth and desire flexibility, universal life could be a better fit. Always assess your comfort level with risk and the level of management you're willing to undertake for your policy.

Summary

Choosing the right life insurance policy is a crucial decision that impacts your family's financial security. Term life insurance offers affordable coverage for a specific period, ideal for temporary needs and budget constraints, without building cash value. Whole life insurance provides lifelong coverage with guaranteed cash value growth and fixed premiums, offering stability and a savings component for permanent needs. Universal life insurance combines lifelong coverage with greater flexibility in premiums and death benefits, and its cash value growth is tied to interest rates, making it suitable for those whose needs might evolve. Each policy type serves distinct purposes, and understanding their individual characteristics is paramount to selecting the best option to protect your loved ones and achieve your long-term financial objectives. It is always advisable to consult with a qualified financial advisor to tailor a solution that perfectly matches your unique situation.

Comprehension questions

What are the main characteristics that differentiate term life insurance from permanent life insurance?How does the cash value component of whole life insurance function, and what are its primary benefits to the policyholder?What makes universal life insurance more flexible than whole life insurance, and what potential risks are associated with this flexibility?What key personal and financial factors should individuals consider when selecting the most suitable life insurance policy for their needs?

What are the main characteristics that differentiate term life insurance from permanent life insurance?How does the cash value component of whole life insurance function, and what are its primary benefits to the policyholder?What makes universal life insurance more flexible than whole life insurance, and what potential risks are associated with this flexibility?What key personal and financial factors should individuals consider when selecting the most suitable life insurance policy for their needs?