How Insurance Provides Security Against Life's Unpredictability

- -->> 2. How Insurance Provides Security Against Life's Unpredictability

What you'll learn

Understanding diverse life risksThe fundamental principle of insuranceVarious types of insurance coverageInsurance's role in financial security and peace of mind

Understanding diverse life risksThe fundamental principle of insuranceVarious types of insurance coverageInsurance's role in financial security and peace of mindLife is an unpredictable journey, filled with moments of joy, challenge, and unforeseen circumstances. While we all hope for smooth sailing, the reality is that risks are an inherent part of existence. From sudden illnesses and accidents to natural disasters and property damage, various events can derail our financial stability and peace of mind. This is where insurance steps in, acting as a crucial safety net designed to mitigate the financial impact of these uncertainties, offering a layer of protection that allows individuals and families to navigate life's inevitable bumps with greater confidence.

Understanding Risk: The Foundation of Insurance

Risk is defined as the possibility of suffering harm or loss. It's an ever-present element in our personal, professional, and financial lives. Some risks are relatively minor, causing inconvenience, while others can be catastrophic, leading to significant financial burden or even permanent life changes. The human desire to minimize these adverse impacts has led to the development of sophisticated risk management tools, with insurance being one of the most effective.

Recognizing different types of risks is the first step in understanding the value of insurance. These can include:

- Personal Risks: Illness, injury, disability, death, unemployment. These directly affect an individual's health, income, or earning capacity.

- Property Risks: Damage or loss to assets like homes, cars, or other valuables due to fire, theft, natural disasters, or accidents.

- Liability Risks: The potential for being held legally responsible for harm or damage caused to another person or their property.

Each of these risk categories presents unique financial challenges that, without proper planning, could lead to severe hardship.

The Core Concept: How Insurance Operates

At its heart, insurance is a mechanism for transferring risk. Instead of bearing the full financial weight of a potential loss yourself, you transfer that risk to an insurance company. In return, you pay a regular premium. The fundamental principle is one of collective security: many individuals contribute small amounts into a common pool, and this pool is then used to compensate the few who experience a covered loss.

This pooling of resources allows insurance companies to spread the risk across a large number of policyholders. Actuaries, who are experts in statistics and risk, calculate the probability of certain events occurring and determine appropriate premium rates. This ensures that the collective premiums are sufficient to cover anticipated claims and operational costs, while also allowing the company to remain solvent and profitable.

When a policyholder experiences an event covered by their policy, they file a claim. If the claim is approved, the insurance company provides financial compensation, as stipulated in the policy contract, helping the individual or entity recover from the loss without facing ruinous out-of-pocket expenses.

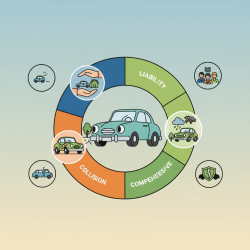

Diverse Shields: Types of Insurance and Their Protection

The insurance industry offers a wide array of products, each tailored to protect against specific risks. Understanding these different types is crucial for building a comprehensive safety net:

- Health Insurance: Covers medical expenses, including doctor visits, hospital stays, prescription drugs, and preventive care. It shields individuals from the exorbitant costs of healthcare, which can quickly deplete savings.

- Life Insurance: Provides a financial payout to designated beneficiaries upon the death of the policyholder. This ensures that dependents are financially supported, covering expenses like mortgages, education costs, and daily living expenses.

- Auto Insurance: Mandatory in most places, it covers damages to your vehicle, damages to other vehicles, and injuries to yourself or others in an accident. It protects against the significant financial liabilities arising from vehicle collisions.

- Homeowner's/Renter's Insurance: Protects your dwelling and personal belongings from perils like fire, theft, vandalism, and certain natural disasters. It also includes liability coverage in case someone is injured on your property.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury. This is vital for maintaining financial stability when your primary income source is interrupted.

- Long-Term Care Insurance: Covers the costs of services not typically covered by health insurance, such as assistance with daily living activities, whether at home, in an assisted living facility, or a nursing home.

Each policy serves a distinct purpose, collectively offering a robust defense against a spectrum of life's financial threats.

Beyond Financial Compensation: The Peace of Mind Factor

While the primary function of insurance is financial protection, its benefits extend far beyond monetary compensation. One of the most significant advantages is the invaluable peace of mind it offers. Knowing that you and your loved ones are protected against potential financial catastrophes allows you to live with less anxiety and greater confidence.

This sense of security frees individuals to pursue their goals, take calculated risks in their careers or investments, and enjoy life without constant worry about what might happen. It transforms potential devastation into manageable setbacks, knowing there's a safety net in place.

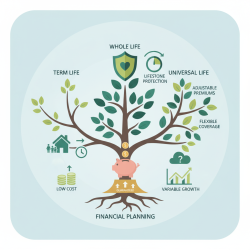

Moreover, insurance plays a vital role in financial planning. It acts as a cornerstone, protecting savings, investments, and assets from being wiped out by unexpected events. Without adequate insurance, a single major illness or accident could erase years of careful financial building, forcing individuals into debt or poverty. With it, financial goals remain attainable, even when challenges arise.

Choosing the Right Coverage: A Strategic Decision

Selecting the appropriate insurance coverage is a highly personal and strategic decision. It requires a careful assessment of individual circumstances, risk tolerance, and financial goals. Factors to consider include:

- Life Stage: A young single professional will have different needs than a married couple with children or someone nearing retirement.

- Financial Dependents: The number of people relying on your income significantly impacts the need for life and disability insurance.

- Assets and Debts: The value of your home, car, savings, and outstanding debts will influence property, auto, and liability coverage.

- Health Status: Pre-existing conditions or family health history might dictate specific health insurance needs.

- Lifestyle and Hobbies: Certain high-risk activities might require specialized coverage.

- Budget: Premiums must be affordable without compromising other financial necessities.

Consulting with a qualified insurance professional can provide invaluable guidance, helping to tailor policies that offer optimal protection without unnecessary costs. Regularly reviewing your policies is also essential, as life circumstances and needs evolve over time.

Summary: Insurance as Your Financial Anchor

In conclusion, insurance is far more than just a financial product; it is an essential component of responsible living and robust financial planning. By pooling resources and transferring individual risks, it provides a powerful safety net against life's inherent uncertainties. From safeguarding health and protecting property to ensuring the financial future of loved ones, various types of insurance offer tailored protection. Beyond monetary compensation, it grants invaluable peace of mind, allowing individuals and families to face the future with greater security and resilience. Understanding risk and strategically choosing the right coverage empowers everyone to build a more secure and stable life.

Comprehension questions

What are the three main categories of risks discussed in the article that insurance aims to mitigate?Explain the core concept of how insurance operates, including the role of pooling resources and premiums.Name at least four different types of insurance mentioned in the article and briefly describe what each protects against.Besides financial compensation, what significant non-monetary benefit does insurance provide to individuals and families?

What are the three main categories of risks discussed in the article that insurance aims to mitigate?Explain the core concept of how insurance operates, including the role of pooling resources and premiums.Name at least four different types of insurance mentioned in the article and briefly describe what each protects against.Besides financial compensation, what significant non-monetary benefit does insurance provide to individuals and families?Review Quiz

Next Lesson

Course Contents : Making Insurance Easy to Understand

- >> 2.

How Insurance Provides Security Against Life's Unpredictability

How Insurance Provides Security Against Life's Unpredictability