Understanding Insurance Basics

- -->> 1. Understanding Insurance Basics

What you'll learn

Understanding Insurance BasicsCore Principles of InsuranceTypes of Insurance CoverageInsurance in Financial Planning

Understanding Insurance BasicsCore Principles of InsuranceTypes of Insurance CoverageInsurance in Financial PlanningIn an unpredictable world, safeguarding one's financial well-being is paramount. Life is full of uncertainties, from unexpected illnesses and accidents to natural disasters and property damage. These events, while unforeseen, can have devastating financial consequences if one is unprepared. This is where insurance steps in, acting as a critical safety net designed to protect individuals and families from significant financial loss. Understanding what insurance is and why it forms an indispensable component of sound financial planning is the first step toward building a secure future.

What Exactly Is Insurance?

At its core, insurance is a contract, represented by a policy, in which an individual or entity receives financial protection or reimbursement against losses from an insurance company. The company pools the risks of its clients, enabling it to pay for the losses of a few from the premiums paid by many. It's essentially a risk management tool where you transfer the financial burden of potential future losses to an insurer in exchange for regular payments, known as premiums.

Think of it as a protective shield. Instead of facing the full financial impact of an unforeseen event alone, you have a collective resource to draw upon. This mechanism transforms potentially catastrophic individual losses into manageable, predictable costs spread across a large group.

The Core Principles of Insurance

Several fundamental principles underpin the concept of insurance, ensuring its functionality and fairness:

- Risk Pooling: Many individuals pay small premiums into a common fund. When a loss occurs to one of them, the fund pays out. This diversification of risk makes insurance financially viable.

- Law of Large Numbers: Insurers use historical data and statistical probabilities to predict the likelihood of claims within a large population, allowing them to set appropriate premium rates.

- Indemnity: The purpose of insurance is to restore the insured to their financial position before the loss occurred, not to allow them to profit from the loss.

- Insurable Interest: The insured must suffer a financial loss if the insured event occurs. You can't insure something you have no financial stake in.

- Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer must act honestly and disclose all material facts relevant to the contract.

Types of Insurance and Their Purpose

The world of insurance is vast, offering specialized coverage for nearly every conceivable risk. Each type addresses a particular financial vulnerability:

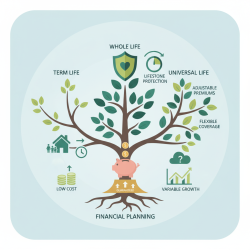

- Life Insurance: Provides a financial payout to beneficiaries upon the death of the insured. It's crucial for income replacement, debt coverage, and ensuring family financial stability.

- Health Insurance: Covers medical expenses, including doctor visits, hospital stays, prescription drugs, and sometimes preventative care. It protects against the exorbitant costs of illness and injury.

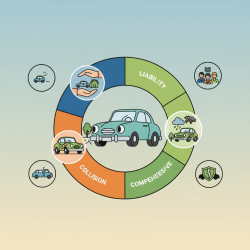

- Auto Insurance: Mandatory in most places, it covers damages and liabilities arising from vehicle accidents, protecting both your assets and those of others.

- Homeowner's/Renter's Insurance: Protects your dwelling and personal belongings against perils like fire, theft, and natural disasters, and provides liability coverage for incidents on your property.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury, preventing financial hardship during a period of no earnings.

- Long-Term Care Insurance: Covers the costs of extended medical care, such as nursing home stays or in-home assistance, often not covered by standard health insurance.

Why Insurance is Crucial for Financial Planning

Insurance is not merely an expense; it's a foundational element of a robust financial plan. It serves several critical roles:

- Risk Mitigation: It acts as a shield against unpredictable events that could otherwise derail your financial progress or deplete your savings. Without insurance, a single major health crisis or property damage could lead to insurmountable debt.

- Preservation of Assets: By transferring risk, insurance protects your hard-earned assets – your home, savings, investments – from being liquidated to cover unexpected losses.

- Peace of Mind: Knowing that you and your loved ones are protected provides immense psychological comfort, allowing you to focus on achieving other financial goals without constant worry.

- Enables Future Planning: With basic risks covered, you are freer to invest in growth opportunities, plan for retirement, or save for education, knowing that a safety net is in place.

- Supports Dependents: Life and disability insurance specifically ensure that your family's financial needs are met even if you are no longer able to provide for them. This includes covering daily expenses, mortgage payments, and future educational costs.

Integrating Insurance into Your Financial Strategy

Effectively incorporating insurance into your financial plan involves careful assessment and strategic decisions. It starts with identifying your unique risks based on your life stage, family situation, assets, and income. Young professionals might prioritize health and disability insurance, while those with families will focus on life insurance. Homeowners will need property and liability coverage.

Regularly reviewing your insurance policies is also vital. Life changes – marriage, children, a new home, career advancement – often necessitate adjustments to your coverage. It's not a one-time decision but an ongoing process to ensure your policies remain aligned with your evolving needs and financial goals. Comparing policies from different providers can also help ensure you get adequate coverage at competitive rates, optimizing your insurance portfolio for maximum protection and value.

Summary

This article explored the fundamental concept of insurance, defining it as a contractual agreement for financial protection against losses. We delved into the core principles that govern its operation, such as risk pooling and indemnity, which highlight its role in spreading financial burdens. A detailed overview of various insurance types, from life and health to auto and homeowner's, illustrated their specific purposes in mitigating different risks. Crucially, the discussion emphasized why insurance is an indispensable component of sound financial planning, serving to protect assets, provide peace of mind, and enable future financial growth by mitigating the impact of unforeseen events.

Comprehension questions

What is the fundamental definition of insurance and how does it function as a risk management tool?Name and briefly explain three core principles that underpin the concept of insurance.List at least four different types of insurance mentioned in the article and state their primary purpose.Explain why insurance is considered a crucial component of sound financial planning, detailing at least two reasons.

What is the fundamental definition of insurance and how does it function as a risk management tool?Name and briefly explain three core principles that underpin the concept of insurance.List at least four different types of insurance mentioned in the article and state their primary purpose.Explain why insurance is considered a crucial component of sound financial planning, detailing at least two reasons.Review Quiz

Next Lesson

Course Contents : Making Insurance Easy to Understand

- >> 1.

Understanding Insurance Basics

Understanding Insurance Basics