Auto Insurance Basics and Key Coverages

- -->> 4. Auto Insurance Basics and Key Coverages

What you'll learn

Liability Coverage EssentialsVehicle Protection: Collision & ComprehensiveUninsured/Underinsured Motorist ProtectionMedical Payments and Other Coverages

Liability Coverage EssentialsVehicle Protection: Collision & ComprehensiveUninsured/Underinsured Motorist ProtectionMedical Payments and Other CoveragesNavigating the world of auto insurance can feel overwhelming, with its myriad of terms, policies, and options. However, understanding the core components of an auto insurance policy is fundamental to protecting yourself, your passengers, your vehicle, and your financial well-being on the road. This article will demystify the essential coverages that form the bedrock of most policies: liability, collision, and comprehensive insurance, along with other crucial protections that drivers should consider.

The Foundation: Understanding Liability Coverage

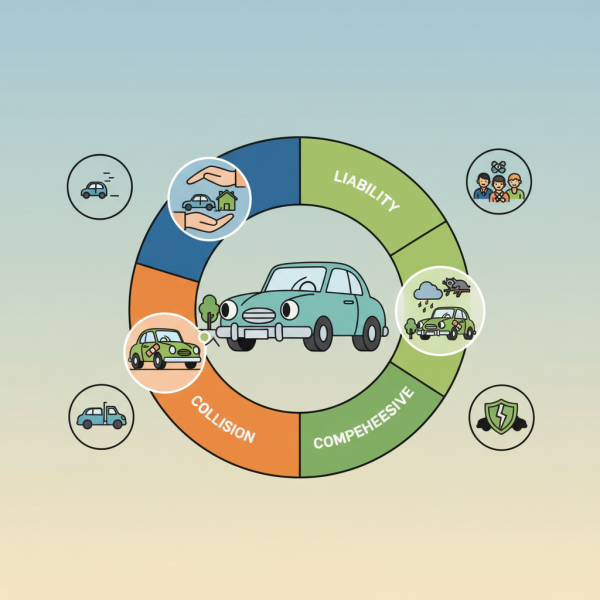

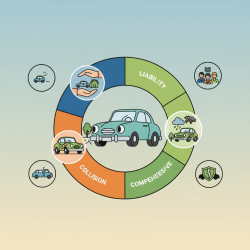

Liability coverage is arguably the most critical component of any auto insurance policy and is legally required in almost every state. Its primary purpose is to cover damages and injuries you might cause to other people or their property in an accident where you are at fault. It doesn't pay for your own injuries or vehicle damage.

Liability coverage is typically split into two main parts:

- Bodily Injury Liability: This covers medical expenses, lost wages, and pain and suffering for anyone injured in an accident you cause. It also covers legal fees if you are sued. Policies usually list two numbers for bodily injury, for example, "$25,000/$50,000". The first number represents the maximum payout for a single person's injuries in an accident, while the second number is the maximum payout for all injuries in a single accident.

- Property Damage Liability: This pays for damage you cause to someone else's property, such as their vehicle, fences, buildings, or other structures. A third number in liability limits, such as "$25,000/$50,000/$10,000", represents the maximum payout for property damage per accident. Choosing higher liability limits is always recommended to protect your assets, as you could be personally responsible for costs exceeding your policy limits.

Protecting Your Vehicle: Collision Coverage

While liability protects others, collision coverage is designed to protect your own vehicle. This type of coverage pays for damage to your car resulting from a collision with another vehicle or an object, regardless of who is at fault. This includes hitting a tree, a pole, or another car.

Collision coverage typically comes with a deductible, which is the amount you agree to pay out of pocket before your insurance company starts to pay. Common deductibles range from $250 to $1,000 or more. A higher deductible usually results in a lower premium, but it means you'll pay more upfront if you need to file a claim. Collision coverage is often required by lenders if you have a car loan or lease, as it protects their investment in your vehicle.

Beyond Accidents: Comprehensive Coverage

Comprehensive coverage protects your vehicle from damages not caused by a collision. It's often referred to as "other than collision" coverage. This includes a wide range of incidents, such as:

- Theft

- Vandalism

- Fire

- Falling objects (e.g., tree branches)

- Impact with an animal (e.g., deer)

- Natural disasters (e.g., floods, hail, windstorms)

Like collision coverage, comprehensive coverage also typically has a deductible. It's an important coverage to consider, especially if your car is relatively new, valuable, or if you live in an area prone to severe weather or higher theft rates. If your car is older and has a low market value, the cost of comprehensive coverage might outweigh its potential benefits.

Other Essential Coverages

While liability, collision, and comprehensive are the big three, several other coverages offer valuable additional protection.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

Despite legal requirements, many drivers operate vehicles without sufficient insurance. UM/UIM coverage protects you if you're involved in an accident with a driver who has no insurance (uninsured) or not enough insurance to cover your damages (underinsured). This coverage can pay for your medical bills, lost wages, and, in some cases, damage to your vehicle, depending on your state and policy specifics. It's a highly recommended protection given the prevalence of uninsured drivers.

Medical Payments (MedPay) or Personal Injury Protection (PIP)

These coverages pay for medical expenses for you and your passengers, regardless of who is at fault for an accident. MedPay covers medical bills and funeral expenses, while PIP (often found in "no-fault" states) can be more extensive, covering medical expenses, lost wages, and essential services like childcare if you're unable to perform them due to injury. The availability and specifics of MedPay and PIP vary significantly by state.

Roadside Assistance and Rental Reimbursement

These are optional but convenient add-ons. Roadside assistance covers services like towing, flat tire changes, jump-starts, and lockout services. Rental reimbursement pays for a rental car while your vehicle is being repaired after a covered claim, ensuring you have transportation during that time. While not critical for financial protection, they offer peace of mind and practical support.

Summary

Understanding auto insurance basics is crucial for every driver. Liability coverage protects others from damages you cause, while collision and comprehensive coverages safeguard your own vehicle against various perils, from accidents to theft and natural disasters. Beyond these core protections, considering coverages like Uninsured/Underinsured Motorist, Medical Payments or PIP, and convenient add-ons like Roadside Assistance and Rental Reimbursement can provide a more complete safety net. Reviewing your needs and regularly assessing your policy ensures you have the right level of protection for your driving habits and financial situation.

Comprehension questions

What is the primary purpose of liability coverage in an auto insurance policy, and what two main parts does it typically include?How do collision and comprehensive coverages differ in terms of the types of damages they cover for your own vehicle?Why is Uninsured/Underinsured Motorist (UM/UIM) coverage considered essential, even if you already have basic liability insurance?In what types of states might you find Personal Injury Protection (PIP) coverage, and what additional benefits can it offer compared to Medical Payments (MedPay)?

What is the primary purpose of liability coverage in an auto insurance policy, and what two main parts does it typically include?How do collision and comprehensive coverages differ in terms of the types of damages they cover for your own vehicle?Why is Uninsured/Underinsured Motorist (UM/UIM) coverage considered essential, even if you already have basic liability insurance?In what types of states might you find Personal Injury Protection (PIP) coverage, and what additional benefits can it offer compared to Medical Payments (MedPay)?Review Quiz

Next Lesson

Course Contents : Making Insurance Easy to Understand

- >> 4.

Auto Insurance Basics and Key Coverages

Auto Insurance Basics and Key Coverages