Social Security Optimization to Maximize Your Lifetime Payout

What you'll learn

Full Retirement Age significanceStrategies for early claimingBenefits of delayed claimingSpousal and survivor benefit considerations

Full Retirement Age significanceStrategies for early claimingBenefits of delayed claimingSpousal and survivor benefit considerationsFor many individuals, Social Security represents a cornerstone of their retirement income, yet navigating its complexities to maximize benefits can feel like deciphering a cryptic puzzle. Deciding when to claim your Social Security benefits is one of the most significant financial decisions you'll make, impacting your lifetime income stream and potentially the financial security of your loved ones. This guide aims to demystify the process, providing insights and strategies to help you make an informed choice that aligns with your financial goals and maximizes your lifetime payout.

Understanding Your Social Security Benefits

Social Security benefits are calculated based on your 35 highest-earning years. The longer you've worked and paid Social Security taxes, and the higher your earnings were, the greater your potential benefit. However, the age at which you choose to start receiving those benefits profoundly affects the monthly amount you receive.

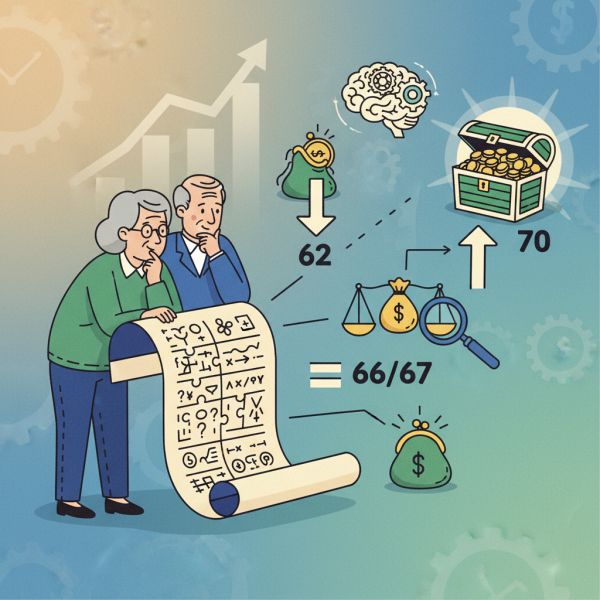

Your "full retirement age" (FRA) is a crucial concept. It's the age at which you're entitled to 100% of your primary insurance amount (PIA). This age varies depending on your birth year. For those born in 1943 through 1954, FRA is 66. It gradually increases for later birth years, reaching 67 for anyone born in 1960 or later.

Understanding your FRA is essential because claiming benefits before it results in a permanent reduction, while delaying benefits past your FRA can significantly increase your monthly payment.

The Impact of Claiming Early

You can start claiming Social Security benefits as early as age 62. While this might seem appealing for those eager to retire or needing income, it comes with a significant drawback: a permanent reduction in your monthly benefit.

For example, if your FRA is 67 and you claim at 62, your monthly benefit could be reduced by up to 30%. This reduction is permanent and will apply for the rest of your life. This means you would need to live many years beyond the break-even point to justify claiming early, assuming a higher monthly payment later on.

There are valid reasons why someone might choose to claim early:

- Immediate financial need or unemployment.

- Poor health and a shortened life expectancy.

- To allow a spouse to delay their own higher benefit.

- Funding other investments that could potentially grow faster than the delayed Social Security benefits.

However, it's critical to weigh these immediate needs against the long-term impact on your lifetime income, especially if you anticipate living a long life.

The Benefits of Delaying Social Security

On the other end of the spectrum is delaying your Social Security benefits past your Full Retirement Age, up to age 70. For each year you delay claiming past your FRA, your monthly benefit increases by approximately 8%. This is known as Delayed Retirement Credits (DRCs).

These credits stop accruing at age 70, so there's no financial advantage to delaying beyond that point. Delaying from FRA to age 70 can result in a monthly benefit that is 24% to 32% higher than your FRA benefit, depending on your FRA. This is a substantial guaranteed annual return that is hard to beat in today's investment landscape without taking on significant risk.

Consider the power of this increase:

- If your FRA benefit is $2,000 at age 67, delaying to age 70 could boost your monthly payment to approximately $2,480. That's an extra $480 per month, or $5,760 per year, for the rest of your life.

- This increased payment is also subject to Cost-of-Living Adjustments (COLAs), meaning the higher base amount will grow even more over time.

Delaying is often the optimal strategy for those who are in good health, have sufficient other retirement funds to cover expenses until age 70, or wish to provide a higher survivor benefit for their spouse.

Key Factors in Your Claiming Decision

The "best" time to claim Social Security isn't one-size-fits-all. It depends heavily on your unique circumstances:

Health and Life Expectancy

If you anticipate a shorter life expectancy due to health issues, claiming earlier might make sense to receive benefits for more years, even if the monthly amount is lower. Conversely, if you expect to live well into your 80s or 90s, delaying can significantly increase your total lifetime payout.

Other Retirement Income and Savings

Do you have enough saved in 401(k)s, IRAs, or other investments to comfortably bridge the gap if you delay Social Security? If not, claiming earlier might be a necessity. If you do, using other assets to live on while your Social Security benefit grows can be a powerful strategy.

Spousal Benefits

If you are married, your claiming decision impacts your spouse. A higher earner delaying their benefit can provide a much larger survivor benefit for the surviving spouse, which is especially important if one spouse has a significantly lower earning record or none at all.

Need for Income

Ultimately, your immediate financial needs play a role. If you are struggling to cover essential expenses without Social Security, waiting might not be a viable option. However, explore all alternatives before making a hasty decision that reduces your long-term security.

Spousal and Survivor Benefit Strategies

For married couples, optimizing Social Security often involves coordinating both spouses' claiming strategies. A common approach for couples where one spouse has significantly higher lifetime earnings is for the higher earner to delay their benefits until age 70. This maximizes their primary benefit, which then becomes the basis for the survivor benefit their spouse would receive if the higher earner passes away first. The lower-earning spouse might claim their own benefit earlier, or even claim a spousal benefit based on their partner's record once their partner claims.

Spousal benefits can be up to 50% of the higher earner's Full Retirement Age benefit. A spouse can claim their own benefit or a spousal benefit, whichever is higher, but generally not both simultaneously at their maximum. Understanding these rules is critical for couples.

Survivor benefits are also key. When one spouse dies, the surviving spouse can typically receive the higher of their own benefit or the deceased spouse's benefit. By maximizing the higher earner's benefit, you're also maximizing the potential survivor benefit, providing greater financial protection for the remaining spouse.

Tools and Professional Advice

The Social Security Administration (SSA) offers valuable resources, including your personal "my Social Security" account, which provides estimates of your future benefits at different claiming ages. There are also numerous online calculators and financial planning tools designed to help you project your lifetime payout based on various scenarios.

For complex situations, or if you simply want personalized guidance, consulting with a qualified financial advisor specializing in retirement planning can be incredibly beneficial. They can help you analyze your specific financial situation, health, and family needs to craft a tailored claiming strategy.

Summary of Key Takeaways

Optimizing your Social Security benefits is a powerful way to enhance your retirement security. While claiming early at age 62 provides immediate income, it comes with a permanent reduction in monthly benefits. Delaying your claim past your Full Retirement Age up to age 70 offers significant guaranteed increases through Delayed Retirement Credits, which can lead to a substantially higher lifetime payout and improved survivor benefits for a spouse. Your personal health, other retirement savings, and marital status are critical factors to consider in making this important decision. Leverage online resources and consider professional advice to develop a strategy that aligns best with your unique financial journey.

Comprehension questions

What are the primary advantages and disadvantages of claiming Social Security benefits at age 62?How do Delayed Retirement Credits work, and what is the maximum age at which they stop accruing?For married couples, what is a key strategy involving the higher earner to maximize survivor benefits?

What are the primary advantages and disadvantages of claiming Social Security benefits at age 62?How do Delayed Retirement Credits work, and what is the maximum age at which they stop accruing?For married couples, what is a key strategy involving the higher earner to maximize survivor benefits?