Consolidating High-Interest Debt

What you'll learn

Debt Consolidation StrategiesPersonal Loan ApplicationsCredit Card Balance TransfersFinancial Management Tips

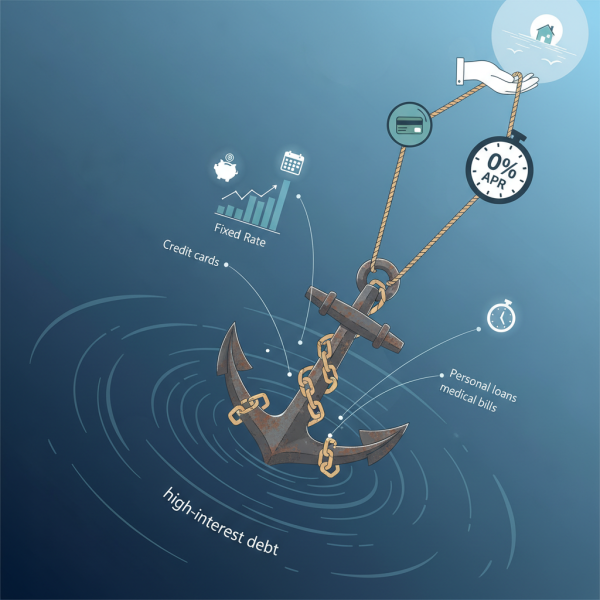

Debt Consolidation StrategiesPersonal Loan ApplicationsCredit Card Balance TransfersFinancial Management TipsHigh-interest debt can feel like a heavy anchor, dragging down your financial progress and creating a constant sense of stress. Whether it's from credit cards, old personal loans, or other sources, the high interest rates mean a significant portion of your monthly payment goes directly to interest, making it incredibly difficult to pay down the principal. This cycle can be disheartening, but there are powerful strategies available to help you take control. Consolidating high-interest debt is one such strategy, offering a pathway to simplify your payments, potentially lower your interest rates, and accelerate your journey towards financial freedom. This article will explore when and how to effectively utilize personal loans and balance transfers to achieve these goals.

Before diving into solutions, it's important to understand the enemy. High-interest debt typically refers to financial obligations with annual percentage rates (APRs) that are significantly above the prime rate, often seen with credit cards or certain payday loans. These high rates mean that even making minimum payments barely touches the principal amount, trapping you in a long-term debt cycle. Recognizing this problem is the first step towards solving it.

Debt consolidation is essentially combining multiple debts into a single, new debt. The primary appeal lies in its ability to simplify your financial life. Instead of juggling several due dates and interest rates, you have one payment to track. More importantly, if done correctly, consolidation can significantly lower your overall interest rate, meaning more of your payment goes towards reducing the actual debt, saving you money and helping you become debt-free faster.

Personal Loans for Debt Consolidation

A personal loan is an unsecured loan, meaning it doesn't require collateral like a house or car. You borrow a lump sum from a bank, credit union, or online lender and repay it in fixed monthly installments over a set period, typically 1 to 5 years, with a fixed interest rate. When used for consolidation, the loan funds are used to pay off your existing high-interest debts.

Personal loans are particularly effective if you have multiple types of high-interest debt, such as several credit cards, medical bills, or old store financing. They are also a strong option if your credit score is good or excellent, as this will qualify you for the most favorable interest rates. If you prefer the predictability of a fixed monthly payment and a clear end date for your debt, a personal loan can be an ideal solution.

Qualifying for a personal loan typically involves a review of your credit score, income, debt-to-income ratio, and employment history. Lenders want to see that you have a stable financial situation and a history of responsible borrowing. The application process usually involves providing personal and financial information, often accompanied by a "soft" credit check initially, followed by a "hard" inquiry if you formally apply. It's wise to shop around and compare offers from several lenders.

- Pros: Fixed interest rate and monthly payment provide predictability; clear payoff date; can consolidate various types of debt; often results in a lower overall interest rate compared to credit cards.

- Cons: Requires a good to excellent credit score for the best rates; approval can be challenging for those with poor credit; missing payments can severely damage your credit; may involve origination fees, though many lenders offer no-fee loans.

Balance Transfers with Credit Cards

A balance transfer involves moving debt from one or more high-interest credit cards to a new credit card, often one that offers a promotional 0% APR period for an introductory period, usually 6 to 21 months. The goal is to pay down as much of the principal as possible during this interest-free window.

Balance transfers are best suited for individuals with primarily credit card debt and a disciplined approach to managing finances. They are especially beneficial if you are confident you can pay off a significant portion, or even all, of the transferred balance before the promotional 0% APR expires. A strong credit score is also essential to qualify for the most attractive balance transfer offers.

To qualify for a balance transfer card, you generally need a good credit score and a low existing debt-to-income ratio. Lenders will assess your creditworthiness to determine the credit limit they can offer you, which must be high enough to cover the debt you wish to transfer. The application process is similar to applying for any new credit card, where you indicate your intention to transfer balances from existing accounts.

- Pros: Opportunity to pay zero interest for an introductory period, allowing payments to go entirely to principal; can significantly reduce the cost of debt if paid off on time; simplifies payments to one card.

- Cons: Typically involves a balance transfer fee (usually 3-5% of the transferred amount); if not paid off during the promotional period, the interest rate can jump significantly, often to a high variable APR; temptation to incur new debt on the old cards; strict deadlines for the introductory rate.

Choosing the Right Strategy

Deciding between a personal loan and a balance transfer depends on several personal financial factors. Your credit score is paramount: better scores unlock better rates for both. The amount of debt you have is also key; large, varied debts might favor a personal loan, while smaller credit card balances are prime for a balance transfer. Your repayment discipline is crucial. Can you pay off a balance transfer before the promotional rate expires, or do you need the fixed, steady payment of a personal loan? Always compare the total cost, including fees, for each option.

Important Considerations Before Consolidating

Debt consolidation is a tool, not a magic bullet. Before you consolidate, critically examine why you accumulated high-interest debt in the first place. Was it overspending, unexpected emergencies, or poor budgeting? Unless you address these underlying behaviors, you risk falling back into debt, potentially even deeper. Create a strict budget and commit to sticking to it.

Always read the fine print. Personal loans might have origination fees deducted from the loan amount. Balance transfers almost always include a transfer fee, typically 3-5% of the transferred balance. Factor these costs into your decision-making process to ensure that consolidation truly saves you money.

Maintaining Momentum After Consolidation

Once you've consolidated, the real work of staying debt-free begins. Avoid using the credit cards you've paid off; consider closing them if temptation is too great, or at least cut them up and keep the accounts open for credit history. Stick to your budget, focus on making your new consolidated payment on time, and build an emergency fund so unexpected expenses don't force you back into high-interest debt.

Conclusion

Consolidating high-interest debt through personal loans or balance transfers can be a game-changer for your financial health. Personal loans offer fixed payments and rates for various debts, ideal for those with good credit and a need for structure. Balance transfers provide a 0% APR window for credit card debt, best for disciplined individuals who can pay off balances quickly. Regardless of the method, addressing the root causes of debt and maintaining financial discipline are essential for long-term success. Choose the option that best fits your financial situation and commit to your journey towards financial freedom.

Comprehension questions

What are the two primary methods discussed for consolidating high-interest debt?Under what circumstances might a personal loan be a more suitable option than a balance transfer?What is a crucial factor to consider when evaluating a balance transfer offer, besides the promotional APR?Why is it important to address the underlying spending habits even after successfully consolidating debt?

What are the two primary methods discussed for consolidating high-interest debt?Under what circumstances might a personal loan be a more suitable option than a balance transfer?What is a crucial factor to consider when evaluating a balance transfer offer, besides the promotional APR?Why is it important to address the underlying spending habits even after successfully consolidating debt?