Understanding Your Credit Score for Financial Wellness

What you'll learn

Payment HistoryCredit UtilizationCredit MixCredit Score Improvement Strategies

Payment HistoryCredit UtilizationCredit MixCredit Score Improvement StrategiesUnlocking the Power of Your Credit Score

In today's financial landscape, your credit score acts as a powerful financial passport, influencing everything from the interest rates you pay on loans to your ability to rent an apartment or even secure certain jobs. For those striving to be more financially savvy and eager to uncover smart money-saving strategies, understanding the intricate workings of your credit score is not just beneficial; it's absolutely essential. This deep dive will demystify the factors that move the needle on your credit rating, empowering you with the knowledge to build, maintain, and leverage excellent credit for a more secure financial future.

What Exactly is a Credit Score? Your Financial Report Card

At its core, a credit score is a three-digit number that represents your creditworthiness, essentially a snapshot of your financial reliability. It's a numerical summary derived from the information contained in your credit report, which details your borrowing and repayment history. Lenders use this score to assess the risk involved in lending you money. A higher score indicates a lower risk, making you a more attractive borrower and often qualifying you for better terms and lower interest rates. The two most common scoring models are FICO (Fair Isaac Corporation) and VantageScore, both widely used and relying on similar underlying data points.

Why does this number hold so much weight? Beyond loans and credit cards, a strong credit score can impact your life in numerous ways. It can determine the premium you pay for car and home insurance, influence whether you're approved for a rental property, and in some cases, even be a factor in employment decisions, particularly for roles involving financial responsibility. Recognizing its pervasive influence is the first step toward taking control of your financial destiny.

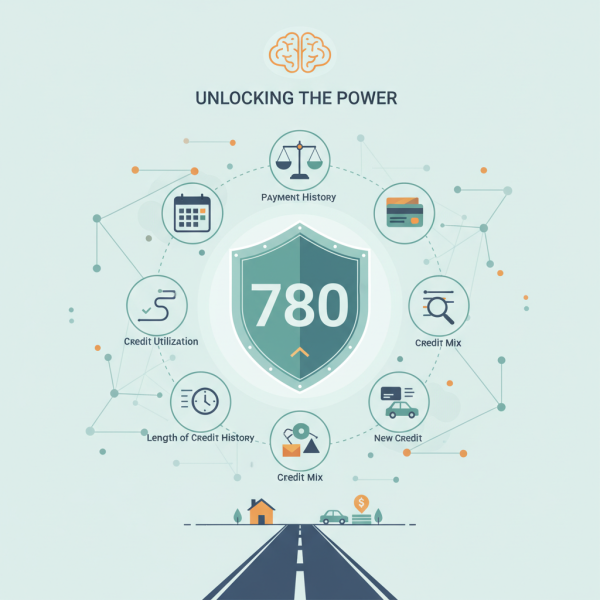

The Five Pillars: Factors That Shape Your Score

Your credit score isn't a random number; it's meticulously calculated based on several key categories of information from your credit report. Understanding these categories is paramount to strategically improving your score.

1. Payment History (Approximately 35% of Your Score)

This is arguably the most critical factor. It reflects whether you pay your bills on time. Every late payment, missed payment, or default can significantly drag down your score, especially if it's recent or a severe delinquency. Conversely, a consistent history of on-time payments across all your accounts (credit cards, loans, mortgages) demonstrates reliability and is the most powerful positive contributor to your score.

Even a single payment that is 30 days past due can cause a noticeable dip. The longer the delinquency and the more frequently it occurs, the more damaging it becomes. Prioritizing timely payments is the golden rule of credit management.

2. Amounts Owed / Credit Utilization (Approximately 30% of Your Score)

This factor examines how much credit you are currently using compared to your total available credit. It's often expressed as a credit utilization ratio. For example, if you have a credit card with a $10,000 limit and carry a $3,000 balance, your utilization is 30%. Financial experts generally recommend keeping your overall credit utilization below 30% across all your revolving accounts. The lower, the better, with many aiming for under 10% for optimal scores.

High utilization signals to lenders that you might be over-reliant on credit, potentially indicating a higher risk. Even if you pay your balance in full each month, if your statement closes with a high balance, it can temporarily affect your score.

3. Length of Credit History (Approximately 15% of Your Score)

This factor considers how long your credit accounts have been open, including the age of your oldest account, the age of your newest account, and the average age of all your accounts. A longer credit history with positive activity generally bodes well for your score, as it provides more data for lenders to assess your reliability over time. This is why it's often advised not to close old, unused credit card accounts, especially if they are your oldest lines of credit, as it can shorten your average credit age.

4. Credit Mix (Approximately 10% of Your Score)

Lenders like to see a healthy mix of different types of credit on your report. This might include both revolving credit (like credit cards) and installment credit (like a car loan, student loan, or mortgage). Demonstrating that you can responsibly manage various credit products indicates financial maturity and diverse experience with debt. However, it's crucial not to open new accounts just to diversify; prioritize responsible usage of existing credit first.

5. New Credit (Approximately 10% of Your Score)

This factor looks at how many new credit accounts you've recently opened and the number of hard inquiries on your report. Each time you apply for new credit (a loan, credit card, or mortgage), a "hard inquiry" is typically made, which can cause a small, temporary dip in your score. While a few inquiries over a year are usually fine, numerous applications in a short period can signal to lenders that you might be in financial distress or are taking on too much new debt too quickly, potentially lowering your score.

Soft inquiries, like checking your own credit score or a pre-qualified offer, do not affect your score.

Decoding Your Credit Report: Your Personal Financial Dossier

While your credit score is the summary, your credit report is the detailed story. It's imperative to regularly review your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. You are entitled to a free copy of your credit report from each bureau once every 12 months.

Why is this crucial? Credit reports can contain errors – incorrect payment statuses, accounts that aren't yours, or outdated information. These inaccuracies can unfairly depress your score. If you find an error, you have the right to dispute it with the credit bureau, which is a vital step in maintaining an accurate and healthy credit profile.

Actionable Strategies to Boost Your Score

Improving your credit score is a journey that requires consistent effort and smart financial habits. Here are actionable steps you can take:

- Pay Every Bill On Time, Every Time: Set up automatic payments or calendar reminders for all your credit accounts. This is the single most impactful action you can take.

- Keep Credit Utilization Low: Aim to use no more than 30% (and ideally under 10%) of your available credit on any revolving account. If you carry a balance, try to pay it down before your statement closing date.

- Don't Close Old Accounts: Even if you don't use them, old credit cards with good payment history contribute positively to your length of credit history and overall available credit. Closing them can shorten your average credit age and increase your utilization ratio.

- Diversify Your Credit Responsibly: Over time, having a mix of revolving and installment credit can be beneficial, but only open new accounts when you genuinely need them and can manage them responsibly.

- Limit New Credit Applications: Space out applications for new credit. Avoid opening multiple new accounts in a short period, as this can lead to several hard inquiries and signal risk.

- Monitor Your Credit Report Regularly: Review your reports annually for errors and unauthorized activity. Promptly dispute any inaccuracies.

- Consider a Secured Credit Card or Credit-Builder Loan: If you're new to credit or rebuilding, these tools can help establish a positive payment history without significant risk to lenders.

The Long Game: Sustaining Good Credit for Lasting Financial Wellness

Building and maintaining a stellar credit score is not a sprint; it's a marathon that yields significant long-term benefits. Consistently practicing good credit habits will lead to an impressive score over time, which, in turn, translates into tangible financial advantages. You'll qualify for lower interest rates on mortgages and car loans, saving you thousands of dollars over the life of these debts. You'll also find it easier to get approved for rental properties, utility services, and even better insurance rates. Beyond the monetary savings, having a strong credit score brings a valuable sense of financial security and peace of mind.

Embrace these strategies, be patient, and commit to consistent financial discipline. Your credit score is a reflection of your financial habits, and by understanding its mechanics, you empower yourself to steer toward a future of greater financial freedom and opportunity.

Summary

This article explored the critical role your credit score plays in your financial life, extending beyond just loans to influence various aspects of daily living. We delved into the five key factors that comprise your credit score: payment history, credit utilization, length of credit history, credit mix, and new credit, highlighting their respective weights and importance. Furthermore, we emphasized the necessity of regularly reviewing your credit report for accuracy and outlined actionable strategies to build and maintain a robust credit score, such as timely payments, keeping utilization low, and responsible credit diversification. By understanding and actively managing these elements, individuals can significantly enhance their financial standing and unlock a myriad of opportunities for savings and stability.

Comprehension questions

What is the most significant factor influencing your credit score?How does credit utilization ratio impact your credit score, and what is a recommended ratio?Why is the length of your credit history important for your credit score?What are two actionable steps individuals can take to improve their credit score?

What is the most significant factor influencing your credit score?How does credit utilization ratio impact your credit score, and what is a recommended ratio?Why is the length of your credit history important for your credit score?What are two actionable steps individuals can take to improve their credit score?